Ask GRAI Anything

Your Real Estate Questions, Answered Instantly via Chat

Help us make GRAI even better by sharing your feature requests.

Most mortgage advice on the internet is either math only or emotion only.

The reality is that your mortgage is a long duration risk contract. It affects your liquidity, job mobility, investing capacity, and how resilient your household is in a bad year.

In 2026, the question is not “Which loan is cheaper.” The question is “Which loan keeps you solvent, flexible, and compounding.”

This guide gives you a decision framework that works across markets, and shows how to model it quickly using a real estate AI platform.

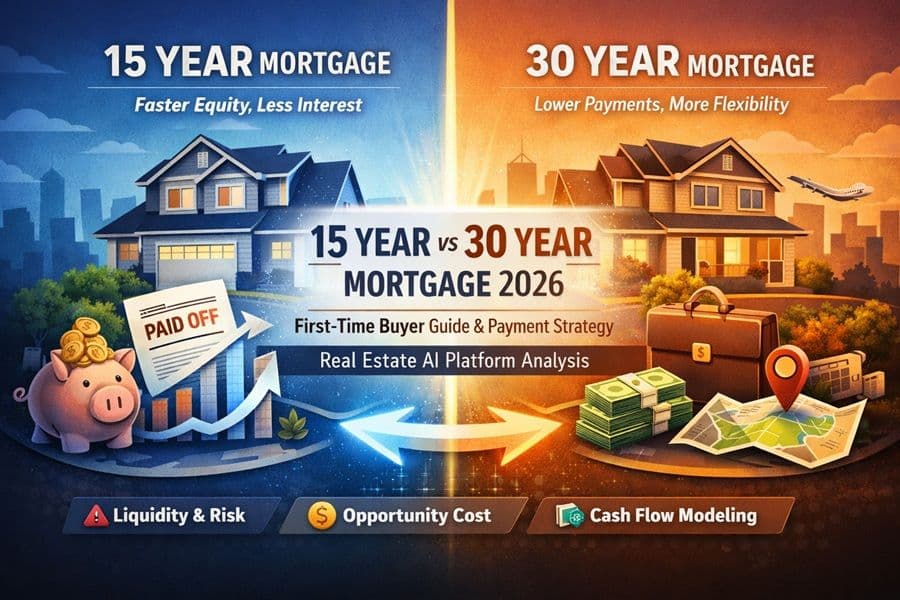

A 15 year mortgage is a forced wealth builder.

A 30 year mortgage is a flexibility engine.

They are not competing products. They solve different risks.

Faster equity build

Lower lifetime interest in most cases

Shorter time to “own it outright”

Less exposure to long term rate risk and refinancing dependency

Lower required monthly payment

More breathing room during income volatility

Higher optionality for investing, career shifts, relocation, or business risk

Ability to pay extra when you want, and stop when life gets messy

The smartest borrowers do not pick one ideology. They pick the structure that fits their risk profile.

Many buyers compare only principal and interest, then get surprised later.

Your true monthly cost is usually closer to this:

Principal and interest

Property taxes

Homeowners insurance

HOA, if applicable

Maintenance reserve

Utilities and recurring operating costs

In many markets, insurance and taxes are no longer minor line items. The “safe” mortgage choice is the one that still leaves room for these costs without turning your budget into a constant emergency.

Before you compare interest savings, run the solvency test.

Ask one blunt question:

If income fell 20% for 6 months, could you still pay the mortgage and keep your life stable without panic selling.

If the answer is no, the 15 year can become a stress amplifier.

A useful rule of thumb for resilience:

This is not about fear. It is about avoiding forced decisions.

Instead of arguing 15 vs 30, compare three strategies:

Best for buyers who want certainty and can comfortably cashflow it.

Best for buyers who need maximum flexibility, but it is often the least efficient if you never deploy the monthly savings into investing or reserves.

This is the “optionality” strategy:

Pay extra principal when your month is strong

Drop to minimum payment if life changes

Preserve flexibility without abandoning acceleration

For many households, Strategy C is the highest quality risk adjusted path.

Model your 15 vs 30 year mortgage with GRAI: https://internationalreal.estate/chat

Most people focus on total interest paid. That matters, but it is not the only metric.

How much cash is left each month after all housing costs and essential expenses.

If you choose a 15 year and your buffer collapses, you may be “winning interest” but losing resilience.

How many months you can survive without income using your liquid reserves.

A longer runway reduces the probability of a forced sale.

What you can do with the monthly difference between a 15 year payment and a 30 year payment.

If you can invest the difference consistently, the 30 year can outperform in net worth terms, even if it costs more interest.

If you cannot invest it consistently, the 15 year often wins because it forces discipline.

maintain the property

cover selling costs

carry the home during listing

qualify for your next mortgage

The numbers below are an example to show how to think, not a claim about current rates.

Assume:

Home price: $500,000

Down payment: 20%

Loan: $400,000

30 year rate: 6.50%

15 year rate: 6.00%

What tends to happen in this type of setup:

The 15 year payment is materially higher each month

The 30 year creates a monthly “difference” you can deploy into reserves, investments, or extra principal

Your best choice depends on what you will actually do with that difference:

Invest it consistently, 30 year can be superior for wealth compounding

Spend it, 15 year is usually superior for forced savings

The decision is behavioral as much as financial.

A 15 year tends to fit best when these are true:

You have stable income, or multiple income streams

You already have a strong emergency fund after closing

You still contribute meaningfully to retirement and investments after the higher payment

You plan to stay long enough for the higher payment to feel worth it

You value certainty more than optionality

If you are buying your “forever home” and you have strong reserves, 15 year can be a clean path to long term security.

A 30 year tends to fit best when these are true:

Your income is variable, commission based, entrepreneurial, or cyclical

You are early career and want mobility

You have childcare, medical, elder care, or other near term cash demands

You want to keep investing aggressively

You want the ability to handle big life changes without refinancing or selling

The 30 year is often the smarter risk contract for first time buyers who want a margin of safety.

A mortgage decision is incomplete if it causes any of the following:

underinsuring the home

skipping maintenance

deferring repairs

draining liquidity to hit a higher monthly payment

A house can become financially dangerous when the payment is manageable but the ownership costs are not.

In 2026, being house rich and cash poor is still the fastest path to regret.

This is exactly where a real estate AI platform can outperform generic advice.

With GRAI, you can model your mortgage choice using your city’s taxes, insurance, HOA reality, and your personal cash flow, then pressure test the downside.

Add these in your workflow before you commit.

GRAI prompts you can ask

“Compare 15 year vs 30 year for my purchase price, down payment, and rate assumptions, include taxes, insurance, HOA, and a maintenance reserve, then show my monthly buffer under each.”

“If I take a 30 year but pay extra like a 15 when possible, show payoff timelines, interest saved, and how many months I can pause extra payments without stress.”

“Run a stress test, income down 20% for 6 months, which mortgage keeps me solvent, show cash runway and required reserves.”

“Rent vs buy for my city using 15 vs 30, include closing costs and conservative home price and rent growth, then show break even year ranges.”

If you want to run it instantly: https://internationalreal.estate/

Not always. It often reduces interest, but a 30 year can win if you invest the payment difference consistently and maintain stronger liquidity.

For many households, yes. It preserves flexibility while allowing acceleration when cash flow is strong.

Monthly buffer, liquidity runway, and the ability to maintain the property without financial strain.

Flexibility tends to matter more. A 30 year can reduce the risk of forced decisions, especially if you might carry the home during a sale or relocate quickly.

In 2026, the best mortgage is not the one that looks cheapest in a spreadsheet during a good year. It is the one that keeps you stable in a bad year while still letting you build wealth in a good year.

Choose 15 year if you can pay it comfortably, keep strong reserves, and still invest.

Choose 30 year if you value optionality, want resilience, or have variable income.

If you want the highest probability “no regrets” path, consider the 30 year paid like a 15 when life allows.

And do not guess. Model it with real numbers using a real estate AI platform.