Ask GRAI Anything

Your Real Estate Questions, Answered Instantly via Chat

Help us make GRAI even better by sharing your feature requests.

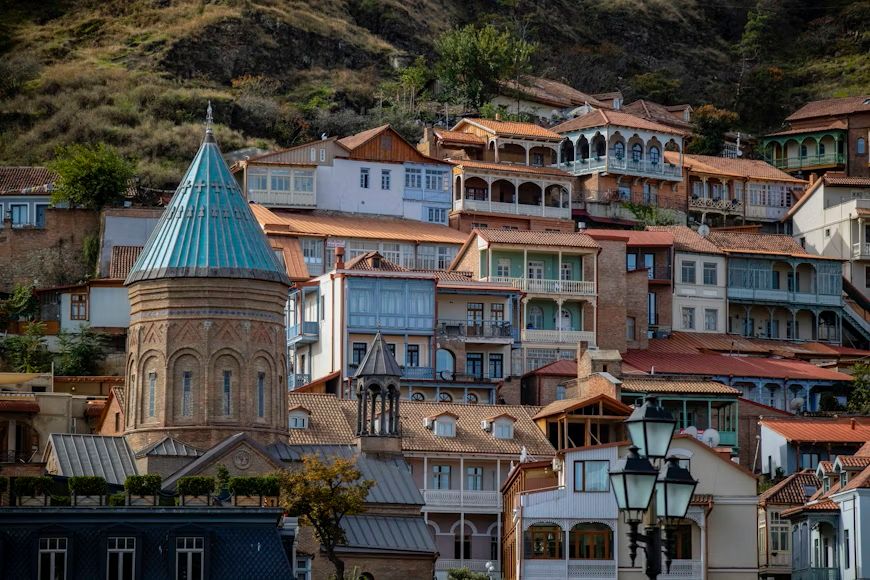

Tbilisi still looks cheap to many foreign buyers and digital nomads, but the market is no longer in its obvious bargain phase. TBC Capital’s March 2026 residential market watch said the average asking sale price in Tbilisi reached $1,348 per square meter, up 7% year over year, while average rental prices were around $10.0 per square meter, down 7% year over year. That combination matters because it signals a more mature, more selective market where sale prices are still climbing but rental momentum has cooled.

At the same time, Georgia remains unusually open to foreign real estate ownership, which keeps Tbilisi attractive to globally mobile buyers. But local commentary has also highlighted rent stress in districts such as Vake, Vera, and Saburtalo, where foreign demand and remote work have made housing harder for locals. The right question in 2026 is no longer whether Tbilisi is cheap. It is whether the city still offers durable property value once the easy hotspot narrative is stripped away.

Tbilisi became globally interesting because it combined several advantages that rarely come together so cleanly:

Low headline property prices

Relatively low living costs

Easy foreign access

A culture and food scene people enjoy

Enough infrastructure for remote work

That mix turned the city into one of the more serious digital nomad and foreign buyer stories outside the standard list of Lisbon, Barcelona, Bali, and Chiang Mai. What makes it more than a travel story is that demand has been strong enough to affect the housing market. Local reporting described rental increases in central districts and growing tension between foreign incomes and local wages, which is exactly the point where a lifestyle trend becomes a real estate market event.

The easiest way to think about Tbilisi in 2026 is this: the city may still be inexpensive in global terms, but it is no longer cheap in the effortless way that made the old thesis so easy.

TBC Capital’s latest watch shows sale prices still rising while rents are softer year over year. That is a very different setup from the earlier “prices are low and rents are exploding” version of the Tbilisi story. When sale prices rise 7% while rents fall 7%, buyers need to think harder about yield compression, exit quality, and how much of the valuation story now depends on future appreciation rather than current cash flow.

One of Tbilisi’s biggest continuing advantages is that Georgia remains comparatively open to foreign ownership. Recent 2026 property guidance aimed at foreign buyers says foreigners can generally purchase apartments and most urban real estate with relatively few restrictions, although agricultural land remains more restricted. Even without relying heavily on secondary guides, Georgia’s legal framework remains broadly investment friendly and protective of property rights, which has been part of the city’s attractiveness for years. The practical effect is clear: it is easier for an internationally mobile buyer to imagine actually owning something in Tbilisi than in many other emerging or high demand cities.

That legal openness is not a small detail. In global real estate, many cities lose buyers not because people dislike the market, but because the ownership path is messy, restricted, or uncertain. Tbilisi still benefits from being relatively legible.

Also Read: Thailand Property for Foreigners in 2026

This is the hard edge of the story.

Local reporting in 2025 described districts like Vake and Saburtalo as seeing one bedroom rents in the $600 to $800 range, a level that may still look reasonable to a Western remote worker earning several thousand euros per month, but which can be punishing for locals on Georgian salaries. Separate reporting said one bedroom rents in popular areas exceeded 1,200 GEL, while the average monthly salary in Georgia was around 2,000 GEL, meaning rent alone could consume more than half of income. These are exactly the kind of numbers that turn a foreign demand story into a local affordability debate.

That does not make Tbilisi “bad” for investors. It does mean that a smart investor should treat local affordability pressure as a real variable, not as background noise.

This is where the Tbilisi story becomes more sophisticated.

There are really two ways to buy into a market like this.

The first is narrative value. You buy because the city is becoming known, people are talking about it, foreigners keep arriving, and you assume that attention alone will keep supporting prices.

The second is real value. You buy because the submarket has durable long stay demand, acceptable building quality, better than average liquidity, and a realistic tenant or buyer pool even if the nomad label fades.

In early hotspot markets, the first kind of value can work surprisingly well. But by the time prices have already moved meaningfully and local housing tension is obvious, the second kind matters much more. Tbilisi in 2026 looks much closer to the second stage.

This may be the most important fact in the whole market right now.

Rising sale prices are not a problem by themselves. Falling rents are not a disaster by themselves. But when they happen together, the burden on the investor changes. The market becomes less forgiving. Buyers can no longer rely on easy rental growth to justify entry prices.

That pushes the investment case toward:

Stronger neighborhood selection

Better unit quality

Longer hold assumptions and

More realistic exit modeling

If the rental market is no longer doing as much work, the wrong asset can look “cheap” on global comparison and still underperform badly.

One of the biggest mistakes foreign buyers make is treating Tbilisi as a single opportunity set. It is not.

Even local commentary pointing to pressure in Vake, Vera, and Saburtalo suggests the market is highly neighborhood specific. Areas that draw remote workers, students, expats, and higher income locals are naturally going to behave differently from districts with thinner demand, weaker walkability, or poorer building quality. If Tbilisi is becoming a more mature property market, then submarket divergence will matter more, not less.

That means the real question is no longer “Should I buy in Tbilisi?” It is “Which part of Tbilisi still has defensible demand once the city level hype is discounted?”

This is the point many global buyers ignore.

A market can have low headline prices and still carry:

Weaker resale depth

Higher building quality variability

Thinner institutional buyer participation

More dependence on foreign sentiment

That is not a reason to avoid Tbilisi. It is a reason to underwrite it properly. A city can remain one of the cheapest serious digital nomad bases and still be a more demanding investment market than buyers first assume.

Local reporting also points to short term rental growth and foreign or tourism linked demand affecting Tbilisi and Batumi. That matters because it shows that Tbilisi’s housing system is being pulled by multiple layers of outside demand at once: digital nomads, expats, tourists, and foreign buyers. When several demand streams overlap, the property market can look stronger for longer, but it can also become more socially and politically exposed.

That makes the market more interesting, but also more fragile if one of those streams cools or rules change.

Use GRAI to compare Tbilisi’s overlapping tourism, expat, and digital nomad demand streams before you commit capital: https://internationalreal.estate/chat

The right framework is not “Is Tbilisi hot?” It is five questions:

A unit that only works for trend driven foreign demand is much weaker than one that also works for local professionals, students, or long stay residents.

That is already close to today’s reality, and it changes yield math sharply.

In a thinner market, exit quality matters more than buyers often assume.

If the foreign buyer story weakens, does the local market still support the asset?

That is the simplest way to separate durable value from hotspot hype.

This is where the GRAI real estate AI platform fits naturally. Tbilisi is not a simple value market and not a simple nomad market.

It sits at the intersection of:

Digital nomad demand

Foreign buyer openness

Local affordability pressure

Sale price growth

Softer rents and

Neighborhood level divergence

A real estate AI platform like GRAI should help people answer questions that basic property portals cannot:

Which Tbilisi districts still have durable rental support

Whether the market is in yield compression

Which properties still work if the hotspot story cools

How Tbilisi compares with Madeira, Bali, and Chiang Mai not on vibe, but on property durability

That is the real difference between trend following and property analysis.

“Compare Tbilisi with Madeira, Bali, and Chiang Mai on property durability, rental support, and digital nomad premium risk.”

“Tell me whether this Tbilisi property still works if rents stay flat but sale prices keep rising."

“Stress test a Tbilisi investment for resale depth, local affordability pressure, and foreign demand slowdown.”

“Explain whether this Tbilisi submarket benefits from durable residential demand or just digital nomad narrative momentum.”

“Compare Vake, Vera, and Saburtalo on long stay rental depth, price resilience, and affordability tension.”

Ask GRAI to stress test any Tbilisi asset for yield compression, resale depth, and neighborhood divergence in seconds: https://internationalreal.estate/chat

By global standards, often yes. But that is not the same thing as saying it is still in its obvious bargain phase. TBC Capital’s March 2026 data shows sale prices are still rising, while rents are softer year over year, which makes the market less forgiving than it used to be.

Generally yes, foreigners can still buy most urban real estate in Georgia with relatively few restrictions, though agricultural land rules are more limited and buyers should always verify the latest legal details for their specific case.

TBC Capital’s March 2026 market watch said the average asking sale price was $1,348 per square meter and the average rental price was $10.0 per square meter.

Because it offers lower relative living costs, easy foreign access, culture, food, and enough infrastructure for remote work. That combination made it one of the more serious non Western European remote work bases.

Yes, local reporting says central districts such as Vake, Vera, and Saburtalo have seen meaningful rent pressure, making housing much harder for many locals on Georgian wages.

It can be, but the city now requires more selective underwriting. Buyers need to focus more on submarket quality, rent durability, and exit depth than they did in the earlier “cheap hotspot” phase.

One of the biggest risks is confusing globally low prices with easy investment quality. Rising sale prices, softer rents, and local affordability pressure mean the wrong asset can underperform even in a city that still looks inexpensive from abroad.

Current local commentary frequently highlights Vake, Vera, and Saburtalo in the context of expat and digital nomad driven rent pressure, which suggests those districts deserve especially careful analysis.

The best comparison is not based on vibe. It should include rental durability, foreign ownership access, local affordability pressure, resale depth, and how much of the premium is narrative versus genuine demand.

Yes. A real estate AI platform like GRAI can compare submarkets, stress test rent and price scenarios, and evaluate whether a property still works if foreign demand or hotspot momentum slows.

Tbilisi in 2026 is still one of the cheapest serious digital nomad bases in the world.

But that is no longer enough of an investment thesis on its own.

The market has moved.

Rents are no longer doing all the work.

Local affordability tension is real.

And the easy version of the story is fading.

That does not mean Tbilisi has lost its edge. It means the edge has changed. The next winners are likely to be the buyers who stop asking whether the city is cheap and start asking which assets still work when the hotspot narrative no longer carries everything.